Your home insurance renewal explained

If you're an existing LV= Car or Home customer, you can be sure you'll always pay the same or less than one of our new customers when you renew.

Your quote will be compared to a new customer price on the same day your renewal was generated, based on the exact same cover.

Why do home insurance prices change?

A rise in the number of claims and how much they cost to resolve can have a major impact on people’s home insurance premiums. Whilst the cost of materials has gone up, a change in premium can be largely due to an increase in the frequency and severity of weather events. Insurers paid out £1.6 billion in claims during the second quarter of 2025 to help homeowners and businesses bounce back from unexpected events and costly disruptions. (Source ABI)

What if my premium has increased and I haven’t made a claim?

Just like other businesses, the increased cost of things affects us and it can also affect our pricing. That’s why, even if you haven’t made a claim, your premium could go up.

When we calculate a price for a policy, we have to factor in what our overall claims costs will be to make sure there’s enough money in the pot for everyone’s claim.

How do home claim costs affect my renewal price?

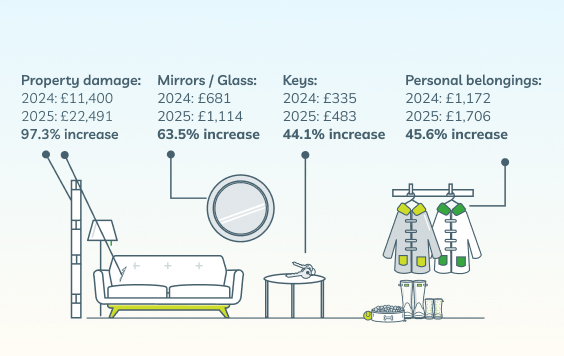

As claims get more expensive, so can home insurance. Our infographic shows how much on average different types of claims cost us in 2024 compared to 2025.

What are some reasons a home insurance cost could rise?

- Building materials: Higher costs of building materials increase the amount we have to spend on repairs.

- Replacing belongings: As the cost to buy things like mobile devices, video games, wooden floors and sofas increases, so does the cost to replace them.

- Severe weather: Storms are getting worse and more frequent. Floods and high winds, like those during storms Bram and Goretti, can see the number of claims and cost of them rise dramatically.

How can I reduce the cost?

Could you increase your voluntary excess? This is the amount of money you pay towards a claim yourself. The higher the excess, the lower your premium is likely to be - just make sure it's an amount you could afford if you needed to make a claim.

What about reviewing your cover and optional extras? Take time to review your renewal documents and make sure you still need the cover and any optional extras.

If you ever need to claim, we’re here to help - please use our online claim form.

It’s really important to us that we continue to put you first and give you the same great service you’ve come to expect. We continue to assess the value of our cover, and an increase in premiums is not something we take lightly.

Take a look at our LV= GI home customer reviews

Thanks to all our customers who have rated us ‘Excellent’ on Trustpilot!

Got a question? We might have answered it here...

We look after over 1 million people like you in the UK so you're in good company

Our customers have rated us as '4.5 Stars - Excellent' on Trustpilot