Your car insurance renewal explained

If you're an existing LV= Car or Home customer, you can be sure you'll always pay the same or less than one of our new customers when you renew.

Your quote will be compared to a new customer price on the same day your renewal was generated, based on the exact same cover.

Why do car insurance prices change?

A rise in the cost to resolve claims has a direct impact on people’s insurance prices. Cars are costing more to repair or replace and premiums can be impacted as a result.

What if I haven’t made a claim?

When we calculate a price for a policy, we have to factor in what our overall claims cost will be to make sure there’s enough money in the pot for everyone’s claim.

Just like other businesses, the increased cost of things affects us and it can also affect our pricing. That’s why, even if you haven't made a claim, your premium could go up.

We continue to assess the value of our cover, and an increase in premiums is not something we take lightly. It’s really important to us that we continue to put you first and give you the same great service you’ve come to expect.

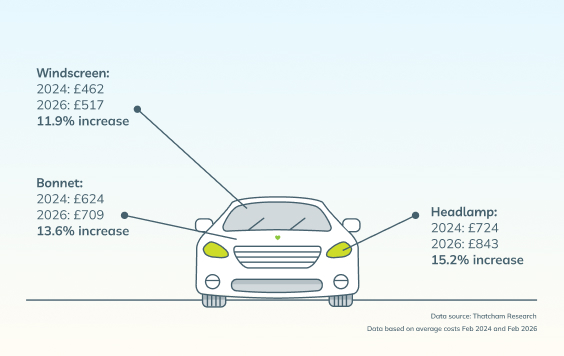

How do car repair costs affect my renewal price?

If car parts or repairs get more expensive, so can car insurance. Our infographic shows how much certain repairs cost in 2024 compared to 2026.

We pay out on over 99% of motor claims.

What are we doing to keep costs down?

We know it’s hard to keep up with the cost of living at the moment and these challenges affect everyone

At LV= we’re doing everything we can to tackle these challenges...

- Maintaining quality while controlling repair costs: We work with a set network of industry leading repairers, exclusively for LV= customers. With pre-agreed prices for repairs and quicker decision making, we ensure the highest standards while controlling costs.

- Expanding our team to get you back on the road: Engineers and specialist engineers for Electric Vehicles are in short supply and many are retiring. We're investing in apprenticeships to grow our engineering team, so we can be there when you need us most.

- Tackling repair delays so you get what you need: We’re working with our suppliers to combat the issue affecting everyone caused by a global shortage of important materials and high-tech car parts, like semi-conductor chips.

Take a look at our LV= car insurance customer reviews

Thanks to all our customers who have rated us ‘Excellent’ on Trustpilot!

What can car insurance claims pay for?

Please check your individual cover as policies can differ.

So, why renew with LV=?

Our friendly call centres are here to help and our Defaqto 5 Star rated insurance reflects the outstanding quality of our cover. You can be confident we offer the highest level of protection for all events.

Got a question? We might have answered it here...

We look after over 2 million people like you in the UK so you're in good company

Our customers have rated us as '4.5 Stars - Excellent' on Trustpilot